A firmer reading from the German ZEW economic sentiment survey, due at 0500 ET, will likely support the euro, while a lower-than-forecast number could see it give up recent gains. On Monday a German PMI survey beat expectations.

The euro rose 0.1 percent against the dollar to $1.3772. The common currency also stayed within reach of a five-year peak against the yen, rising about 0.1 percent to 141.82 yen.

The euro also rose against the Swedish crown after the Riksbank cut the repo rate as expected. The crown fell to a session low of 9.0791 per euro in high volumes after the central bank struck a dovish note by lowering the rate path.

The single currency has shrugged off some poor recent economic data - particularly inFrance - to surprise many analysts and move higher since the summer.

A key driver has been tighter money markets, as banks repay cheap European Central Bank loans. Liquidity usually tightens towards the end of the year anyway, when banks hold off from lending to each other.

This year, another factor driving euro strength is European banks repatriating funds to shore up their capital bases before an ECB Asset Quality Review (AQR). EU banks reduced their assets by 817 billion euros between December 2011 and June 2013, according to the European Banking Authority.

"(Euro/dollar) above $1.35 is not fundamentally justified if you look at what's happening in the U.S. and Europe. But underlying flows are euro-positive," said Carl Hammer, chief currency strategist at SEB in Stockholm.

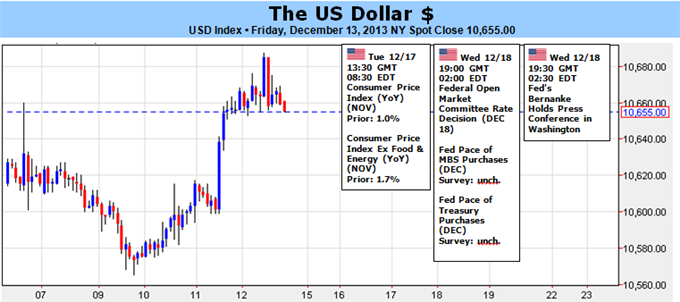

"Obviously everyone is waiting for the Fed decision. We are looking for the Fed to initiate cautious tapering," he said. He expects bond-buying to be reduced by $5-10 billion and the unemployment threshold - when the Fed would consider raising interest rates - to be lowered to 6 percent.

The Fed begins its latest two-day policy meeting on Tuesday. A majority of economists polled by Reuters expect it to taper its huge bond-buying program in March, although the odds on a move this month or next have shortened after a run of upbeat data.

The dollar, which hit a five-year high of 103.925 yen on Friday, was down marginally at 102.97 yen. There was talk among traders of options expiring at the 103 yen level, which could help keep the Japanese currency at these levels.

U.S. economic data continues to suggest improving prospects, with industrial production posting its biggest increase in a year in November, finally pushing industrial output above its pre-recession peak.

"Some of the momentum that we saw in some currencies, like dollar/yen, euro, sterling, it seems to have faded at the moment, which could be partly going into year-end with less liquidity and some profit-taking, which could be limiting moves," said Mitul Kotecha, head of global foreign exchange strategy for Credit Agricole in Hong Kong.

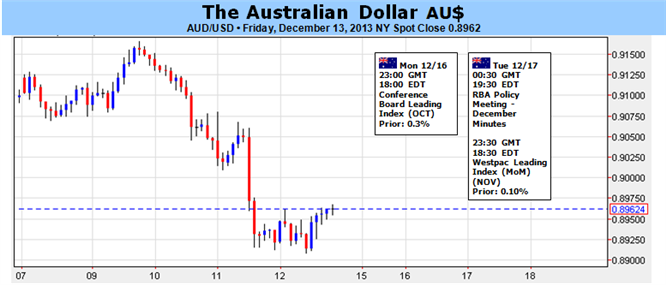

The Australian dollar fell 0.2 percent to $0.8934, heading back towards the more-than-three-month low it hit on Friday, after the release of the minutes of the Reserve Bank of Australia's December 3 policy meeting. The RBA said the Aussie is still uncomfortably high despite the fact it has weakened noticeably over the past month.

Australia's government has also abandoned any intentions of returning to a budget surplus and predicted deficits for the next decade without spending cuts.

Source:http://www.reuters.com